|

Attention! Read the forum rules carefully before posting a topic.

Try to find an answer in Wiki before asking a question.

Submit programming questions in this forum only.

Off topics are strictly forbidden.

Any topics which do not satisfy these rules will be deleted.

| Calculate Indicator prior to candle close |

|

EBMMLuke

|

| Post subject: Calculate Indicator prior to candle close |

Post rating: 0

|

Posted: Sat 06 Nov, 2021, 14:50

Posted: Sat 06 Nov, 2021, 14:50

|

|

User rating: 0

Joined: Mon 04 Nov, 2019, 21:12

Posts: 10

Location: Switzerland,

|

Good day all! My strategy is based in daily candles, which I generate using IFeedDescriptor with custom period. Trading logic and indicator calculation is placed in the onFeedData function. When the strategy is generating an order signal on the close of Friday night, the position won't be opened until Monday, obviously. What I'd like to achieve is keeping the daily timeframe (NY open/close) as is, but check the indicators 15min prior to candle close, so the orders are properly placed. For example: candle start: 3.11. 22:00 EET candle close/start: 4.11. 22:00 EET ==> indicator check 4.11. 21:45 EET candle close: 5.11. 22:00 EET ==> indicator check 5.11. 21:45 EET What would be the best solution to keep the indicator calculation based on the candle above, but checking values earlier? I was thinking about - aggregating 95x 15min candles (24*4 -1), first candle starts with daily open, then feed data array to indicator

- shifting daily candle by 15min (bad solution, as NY hours are not respected anymore)

- others?

Thanks a lot for your help! Cheers, Luke

|

|

|

|

|

|

|

EBMMLuke

|

| Post subject: Re: Calculate Indicator prior to candle close |

Post rating: 0

|

Posted: Thu 11 Nov, 2021, 22:03

|

|

User rating: 0

Joined: Mon 04 Nov, 2019, 21:12

Posts: 10

Location: Switzerland,

|

|

Good evening.

I solved the problem with a combination of daily bars pulled from history plus a custom function for the current day, counting 15min candles.

Works great with indicators with 2D input arrays in the form of double[][].

I'd like to implement it for the ATR as well, which uses a 3D input array in the form of double[][][].

Could someone please advise how to populate these arrays correctly? I didn't find anything in the support board or javadocs.

Help is greatly appreciated!

Cheers, Luke

|

|

|

|

|

|

|

EBMMLuke

|

| Post subject: Re: Calculate Indicator prior to candle close |

Post rating: 0

|

Posted: Fri 12 Nov, 2021, 21:20

|

|

User rating: 0

Joined: Mon 04 Nov, 2019, 21:12

Posts: 10

Location: Switzerland,

|

...and here some code. Most of it is still hardcoded to fiddle around with array length and the like. Just ignore ;o) Populating price array with daily close price data: public double[][][] dataCollection3D() throws JFException {

long prevBarTime = history.getPreviousBarStart(period1d, history.getLastTick(Instrument.EURUSD).getTime());

List<IBar> bars = history.getBars(Instrument.EURUSD, period1d, OfferSide.BID, Filter.WEEKENDS, 99, prevBarTime, 0);

int last = bars.size() - 1; //get array position of last bar

double[][][] closeValues = new double[1][3][100];

for(int i=0; i<=last; i++) { //Inputs for ATR: HLC Price

closeValues[0][0][i] = bars.get(i).getHigh();

closeValues[0][1][i] = bars.get(i).getLow();

closeValues[0][2][i] = bars.get(i).getClose();

}

return closeValues;

}Calculating custom ATR indicator: IIndicator customATR = indicators.getIndicator("ATR");

//set optional inputs

customATR.setOptInputParameter(0, 14);

//set inputs

double[][][] closeValues = dataCollection3D();

//Inputs for ATR: HLC Price 3D, add 15min bar prices

closeValues[0][0][closeValues.length - 1] = bar15min.getHigh();

closeValues[0][1][closeValues.length - 1] = bar15min.getLow();

closeValues[0][2][closeValues.length - 1] = bar15min.getClose();

customATR.setInputParameter(0, closeValues);

//set outputs

double [] resultcustomATR = new double [closeValues.length - 14];

customATR.setOutputParameter(0, resultcustomATR);

//calculate

customATR.calculate(0, closeValues.length - 1);

for(int r=0; r <= resultcustomATR.length; r++) {

console.getOut().println("Custom ATR calc: " + resultcustomATR[r]);

}This code calculates a result, but it's far off the values from the platform ATR. I wrote a method to calculate the ATR according to these formulas https://en.wikipedia.org/wiki/Average_true_range using the input arrays as shown above. It works perfectly and calculates the exact values as the platform ATR. Hence, there must be an issue with the input array or some settings.

|

|

|

|

|

|

|

EBMMLuke

|

| Post subject: Re: Calculate Indicator prior to candle close |

Post rating: 0

|

Posted: Thu 16 Dec, 2021, 14:44

|

|

User rating: 0

Joined: Mon 04 Nov, 2019, 21:12

Posts: 10

Location: Switzerland,

|

Good afternoon! I was proposed a solution for my problem, see the implementation in the code attached. Everything works now as intended, but only for a single instrument. As soon as I subscribe to 2 or more instruments, something messes with my custom SSL indicator (code attached as well). Tests performed so far: - execution time measured for different functions; no abnormalities

- not calling any of the trade execution logic; problem remains

- trying different pair combination (same/different quote currencies aso); problem remains

- checked feeds for indi calculation; numbers are correct

- SSL: add init function to make sure it's on the correct setting

- SSL: longer lookback period to make sure it switched before test period start

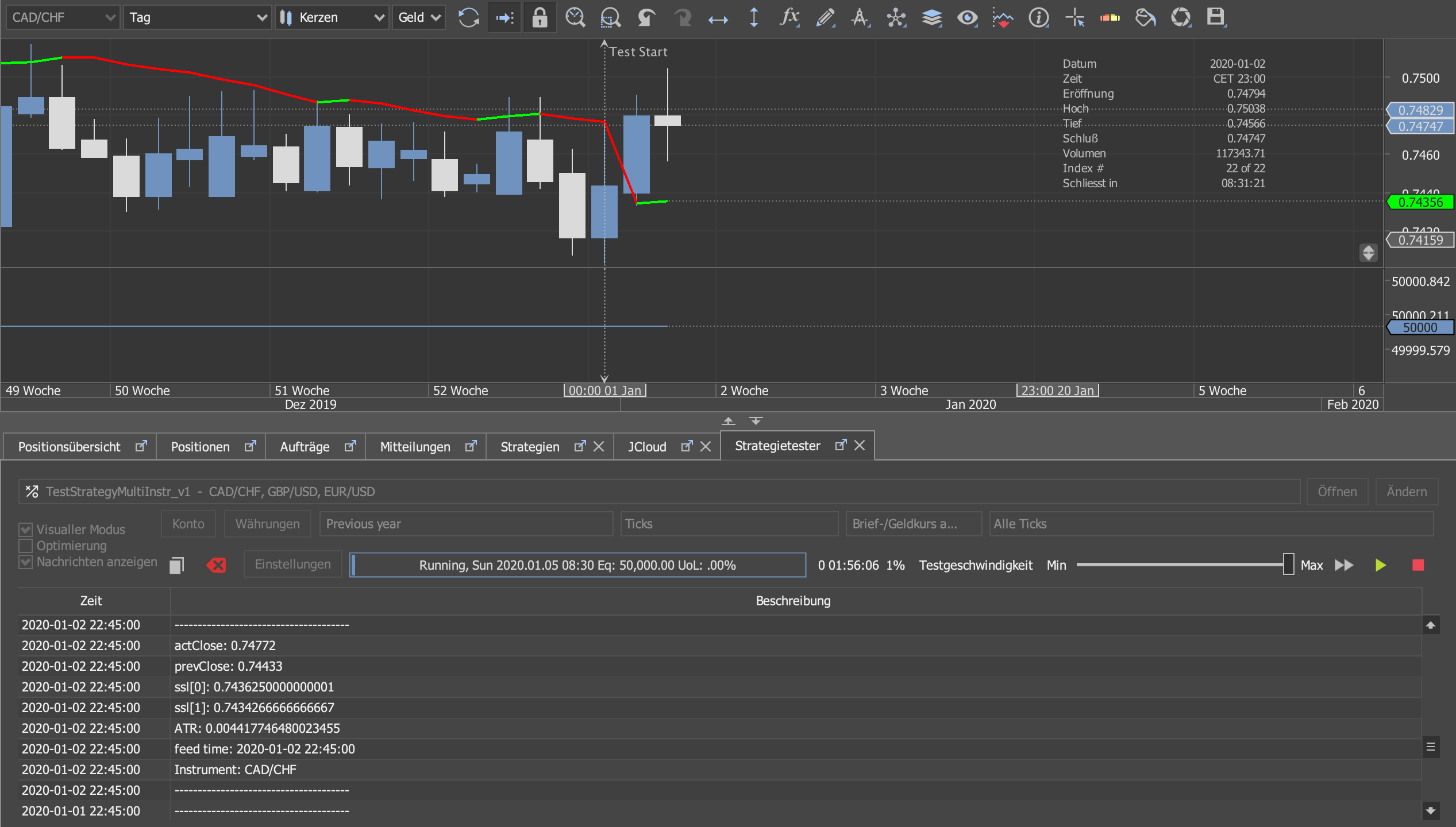

What I think it comes down to is the way I organised the subscription instruments and FeedDescriptors, or how I call the SSL indicator. Probably not the best implementation method? Interestingly, there is no issue with the platform ATR whatsoever. I'm quite new to Java, so please be kind  In the screenshot below you notice the incorrect SSL values. ssl[1] is the actual, ssl[0] the previous. ssl[0] should be 0.74769, but instead the lower SMA value of 0.7436 is calculated. Therefore, a trading signal is not generated as it should have been. Feel free to play around with the instruments and settings to recreate the problem. Thanks, Luke

| Attachments: |

SSL_multiinstr.png [327.77 KiB]

SSL_multiinstr.png [327.77 KiB]

Downloaded 393 times

|

SSL.java [5.21 KiB]

Downloaded 277 times

|

TestStrategyMultiInstr_v1.java [12.96 KiB]

Downloaded 233 times

|

|

DISCLAIMER: Dukascopy Bank SA's waiver of responsability - Documents, data or information available on

this webpage may be posted by third parties without Dukascopy Bank SA being obliged to make any control

on their content. Anyone accessing this webpage and downloading or otherwise making use of any document,

data or information found on this webpage shall do it on his/her own risks without any recourse against

Dukascopy Bank SA in relation thereto or for any consequences arising to him/her or any third party from

the use and/or reliance on any document, data or information found on this webpage.

|

|

|

|

|

|

|

|

EBMMLuke

|

| Post subject: Re: Calculate Indicator prior to candle close |

Post rating: 0

|

Posted: Sun 19 Dec, 2021, 15:08

|

|

User rating: 0

Joined: Mon 04 Nov, 2019, 21:12

Posts: 10

Location: Switzerland,

|

Good afternoon After some more testing I think I've found the problem. It seems, that from the custom SSL indicator just one single instance is used for all instruments, and not one instance for every instrument. As I use a trigger variable in the SSL to determine which SMA band (high, low) to follow, and this trigger seems to be similar for all instruments. This should not be the case of course, as not for all instruments the same band is used at all times. I register the custom indi like this: String indPath = getClass().getAnnotation(CustomIndicators.class).value();

//for multiple indicators split the path with File.pathSeparator

IIndicator indicator = indicators.getIndicatorByPath(indPath);

if(indicator == null){

console.getErr().println("Indicator by path "+indPath+" not registered!");

context.stop();

}

indName = indicator.getIndicatorInfo().getName();

Is there a way to generate an indicator instance for every instrument/feed and call this indi-instance for the respective instru/feed? Something similar as it is done with the FeedDescriptor (see below)? Instrument/Feed subscription instSet = new HashSet<Instrument>();

//instSet.add(Instrument.GBPUSD);

instSet.add(Instrument.EURUSD);

instSet.add(Instrument.AUDUSD);

//instSet.add(Instrument.USDJPY);

//instSet.add(Instrument.CHFJPY);

//instSet.add(Instrument.USDCAD);

//instSet.add(Instrument.NZDUSD);

instSet.add(Instrument.CADCHF);

context.setSubscribedInstruments(instSet);

//subscribe to Feed

feedSet = new HashSet<FeedDescriptor>();

for(Instrument instr : instSet) {

feedSet.add(new TimePeriodAggregationFeedDescriptor(instr, myPeriod, OfferSide.BID, Filter.ALL_FLATS));

}

for(FeedDescriptor feed : feedSet) {

context.subscribeToFeed(feed, this);

}

select correct instrument/feed at onBar method: public void onBar(Instrument instrument, Period period, IBar askBar, IBar bidBar) throws JFException {

//check instrument & if period = 15mins

if (!instSet.contains(instrument) || !period.equals(Period.TEN_SECS)) {

return;

}

//create Feed for instrument

for(FeedDescriptor feed : feedSet) {

if(feed.getInstrument() == instrument) {

myFeedDescriptor = feed;

}

}

//some code....

}

Thanks, Luke

|

|

|

|

|

|

|

Pages: [

1

]

|

|

|

|

|