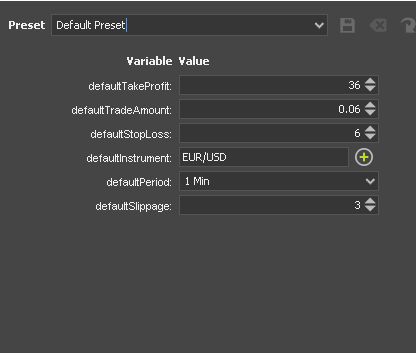

So I have stop loss 6 and take profit 36, but my code only gives me equal stop loss and take profit, so that I can not make any profit.

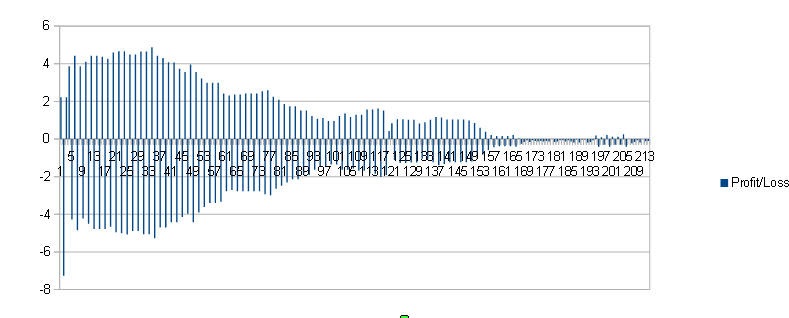

Here is what the results look like. What is wrong?

So the settings and the results do not correlate.

Why can I not set stop loss and take profit so that it actually works?

here is my code

package com.dukascopy.visualforex.visualjforex;

import java.util.*;

import com.dukascopy.api.*;

import java.text.SimpleDateFormat;

import java.util.Calendar;

import java.util.concurrent.CopyOnWriteArrayList;

import java.lang.reflect.*;

import java.math.BigDecimal;

/*

* Created by VisualJForex Generator, version 3.0.9

* Date: 25.12.2021 07:41

*/

public class untitledStrategy1 implements IStrategy {

private CopyOnWriteArrayList<TradeEventAction> tradeEventActions = new CopyOnWriteArrayList<TradeEventAction>();

private static final String DATE_FORMAT_NOW = "yyyyMMdd_HHmmss";

private IEngine engine;

private IConsole console;

private IHistory history;

private IContext context;

private IIndicators indicators;

private IUserInterface userInterface;

@Configurable("defaultTakeProfit:")

public int defaultTakeProfit = 36;

@Configurable("defaultTradeAmount:")

public double defaultTradeAmount = 0.06;

@Configurable("defaultStopLoss:")

public int defaultStopLoss = 6;

@Configurable("defaultInstrument:")

public Instrument defaultInstrument = Instrument.EURUSD;

@Configurable("defaultPeriod:")

public Period defaultPeriod = Period.ONE_MIN;

@Configurable("defaultSlippage:")

public int defaultSlippage = 3;

private Candle LastBidCandle = null ;

private String AccountId = "";

private List<IOrder> PendingPositions = null ;

private double Equity;

private List<IOrder> OpenPositions = null ;

private Tick LastTick = null ;

private String AccountCurrency = "";

private double UseofLeverage;

private IMessage LastTradeEvent = null ;

private int OverWeekendEndLeverage;

private boolean GlobalAccount;

private Candle LastAskCandle = null ;

private int MarginCutLevel;

private List<IOrder> AllPositions = null ;

private double Leverage;

public void onStart(IContext context) throws JFException {

this.engine = context.getEngine();

this.console = context.getConsole();

this.history = context.getHistory();

this.context = context;

this.indicators = context.getIndicators();

this.userInterface = context.getUserInterface();

subscriptionInstrumentCheck(defaultInstrument);

ITick lastITick = context.getHistory().getLastTick(defaultInstrument);

LastTick = new Tick(lastITick, defaultInstrument);

IBar bidBar = context.getHistory().getBar(defaultInstrument, defaultPeriod, OfferSide.BID, 1);

IBar askBar = context.getHistory().getBar(defaultInstrument, defaultPeriod, OfferSide.ASK, 1);

LastAskCandle = new Candle(askBar, defaultPeriod, defaultInstrument, OfferSide.ASK);

LastBidCandle = new Candle(bidBar, defaultPeriod, defaultInstrument, OfferSide.BID);

subscriptionInstrumentCheck(Instrument.fromString("EUR/USD"));

}

public void onAccount(IAccount account) throws JFException {

AccountCurrency = account.getCurrency().toString();

Leverage = account.getLeverage();

AccountId= account.getAccountId();

Equity = account.getEquity();

UseofLeverage = account.getUseOfLeverage();

OverWeekendEndLeverage = account.getOverWeekEndLeverage();

MarginCutLevel = account.getMarginCutLevel();

GlobalAccount = account.isGlobal();

}

private void updateVariables(Instrument instrument) {

try {

AllPositions = engine.getOrders();

List<IOrder> listMarket = new ArrayList<IOrder>();

for (IOrder order: AllPositions) {

if (order.getState().equals(IOrder.State.FILLED)){

listMarket.add(order);

}

}

List<IOrder> listPending = new ArrayList<IOrder>();

for (IOrder order: AllPositions) {

if (order.getState().equals(IOrder.State.OPENED)){

listPending.add(order);

}

}

OpenPositions = listMarket;

PendingPositions = listPending;

} catch(JFException e) {

e.printStackTrace();

}

}

public void onMessage(IMessage message) throws JFException {

if (message.getOrder() != null) {

updateVariables(message.getOrder().getInstrument());

LastTradeEvent = message;

for (TradeEventAction event : tradeEventActions) {

IOrder order = message.getOrder();

if (order != null && event != null && message.getType().equals(event.getMessageType())&& order.getLabel().equals(event.getPositionLabel())) {

Method method;

try {

method = this.getClass().getDeclaredMethod(event.getNextBlockId(), Integer.class);

method.invoke(this, new Integer[] {event.getFlowId()});

} catch (SecurityException e) {

e.printStackTrace();

} catch (NoSuchMethodException e) {

e.printStackTrace();

} catch (IllegalArgumentException e) {

e.printStackTrace();

} catch (IllegalAccessException e) {

e.printStackTrace();

} catch (InvocationTargetException e) {

e.printStackTrace();

}

tradeEventActions.remove(event);

}

}

}

}

public void onStop() throws JFException {

}

public void onTick(Instrument instrument, ITick tick) throws JFException {

LastTick = new Tick(tick, instrument);

updateVariables(instrument);

}

public void onBar(Instrument instrument, Period period, IBar askBar, IBar bidBar) throws JFException {

LastAskCandle = new Candle(askBar, period, instrument, OfferSide.ASK);

LastBidCandle = new Candle(bidBar, period, instrument, OfferSide.BID);

updateVariables(instrument);

OpenatMarket_block_10(1);

}

public void subscriptionInstrumentCheck(Instrument instrument) {

try {

Set<Instrument> instruments = new HashSet<Instrument>();

instruments.add(instrument);

context.setSubscribedInstruments(instruments, true);

} catch (Exception e) {

e.printStackTrace();

}

}

public double round(double price, Instrument instrument) {

BigDecimal big = new BigDecimal("" + price);

big = big.setScale(instrument.getPipScale() + 1, BigDecimal.ROUND_HALF_UP);

return big.doubleValue();

}

public ITick getLastTick(Instrument instrument) {

try {

return (context.getHistory().getTick(instrument, 0));

} catch (JFException e) {

e.printStackTrace();

}

return null;

}

private void OpenatMarket_block_10(Integer flow) {

Instrument argument_1 = defaultInstrument;

double argument_2 = defaultTradeAmount;

int argument_3 = defaultSlippage;

int argument_4 = defaultStopLoss;

int argument_5 = defaultTakeProfit;

String argument_6 = "";

ITick tick = getLastTick(argument_1);

IEngine.OrderCommand command = IEngine.OrderCommand.BUY;

double stopLoss = tick.getBid() - argument_1.getPipValue() * argument_4;

double takeProfit = round(tick.getBid() + argument_1.getPipValue() * argument_5, argument_1);

try {

String label = getLabel();

IOrder order = context.getEngine().submitOrder(label, argument_1, command, argument_2, 0, argument_3, stopLoss, takeProfit, 0, argument_6);

OpenatMarket_block_11(flow);

} catch (JFException e) {

e.printStackTrace();

}

}

private void OpenatMarket_block_11(Integer flow) {

Instrument argument_1 = defaultInstrument;

double argument_2 = defaultTradeAmount;

int argument_3 = defaultSlippage;

int argument_4 = 25;

int argument_5 = defaultTakeProfit;

String argument_6 = "";

ITick tick = getLastTick(argument_1);

IEngine.OrderCommand command = IEngine.OrderCommand.SELL;

double stopLoss = tick.getAsk() + argument_1.getPipValue() * argument_4;

double takeProfit = round(tick.getAsk() - argument_1.getPipValue() * argument_5, argument_1);

try {

String label = getLabel();

IOrder order = context.getEngine().submitOrder(label, argument_1, command, argument_2, 0, argument_3, stopLoss, takeProfit, 0, argument_6);

} catch (JFException e) {

e.printStackTrace();

}

}

class Candle {

IBar bar;

Period period;

Instrument instrument;

OfferSide offerSide;

public Candle(IBar bar, Period period, Instrument instrument, OfferSide offerSide) {

this.bar = bar;

this.period = period;

this.instrument = instrument;

this.offerSide = offerSide;

}

public Period getPeriod() {

return period;

}

public void setPeriod(Period period) {

this.period = period;

}

public Instrument getInstrument() {

return instrument;

}

public void setInstrument(Instrument instrument) {

this.instrument = instrument;

}

public OfferSide getOfferSide() {

return offerSide;

}

public void setOfferSide(OfferSide offerSide) {

this.offerSide = offerSide;

}

public IBar getBar() {

return bar;

}

public void setBar(IBar bar) {

this.bar = bar;

}

public long getTime() {

return bar.getTime();

}

public double getOpen() {

return bar.getOpen();

}

public double getClose() {

return bar.getClose();

}

public double getLow() {

return bar.getLow();

}

public double getHigh() {

return bar.getHigh();

}

public double getVolume() {

return bar.getVolume();

}

}

class Tick {

private ITick tick;

private Instrument instrument;

public Tick(ITick tick, Instrument instrument){

this.instrument = instrument;

this.tick = tick;

}

public Instrument getInstrument(){

return instrument;

}

public double getAsk(){

return tick.getAsk();

}

public double getBid(){

return tick.getBid();

}

public double getAskVolume(){

return tick.getAskVolume();

}

public double getBidVolume(){

return tick.getBidVolume();

}

public long getTime(){

return tick.getTime();

}

public ITick getTick(){

return tick;

}

}

protected String getLabel() {

String label;

label = "IVF" + getCurrentTime(LastTick.getTime()) + generateRandom(10000) + generateRandom(10000);

return label;

}

private String getCurrentTime(long time) {

SimpleDateFormat sdf = new SimpleDateFormat(DATE_FORMAT_NOW);

return sdf.format(time);

}

private static String generateRandom(int n) {

int randomNumber = (int) (Math.random() * n);

String answer = "" + randomNumber;

if (answer.length() > 3) {

answer = answer.substring(0, 4);

}

return answer;

}

class TradeEventAction {

private IMessage.Type messageType;

private String nextBlockId = "";

private String positionLabel = "";

private int flowId = 0;

public IMessage.Type getMessageType() {

return messageType;

}

public void setMessageType(IMessage.Type messageType) {

this.messageType = messageType;

}

public String getNextBlockId() {

return nextBlockId;

}

public void setNextBlockId(String nextBlockId) {

this.nextBlockId = nextBlockId;

}

public String getPositionLabel() {

return positionLabel;

}

public void setPositionLabel(String positionLabel) {

this.positionLabel = positionLabel;

}

public int getFlowId() {

return flowId;

}

public void setFlowId(int flowId) {

this.flowId = flowId;

}

}

}